We have had the very unusual spectacle of Asian Central Banks hypnotized by the snarl of the market cobra unleashing its fangs. While it is a natural human reaction to be thus mesmerized into inaction by a Cobra in the wild, there is little room for further inaction by Asian Central Bankers who stand similarly transfixed by an asset market collapse.

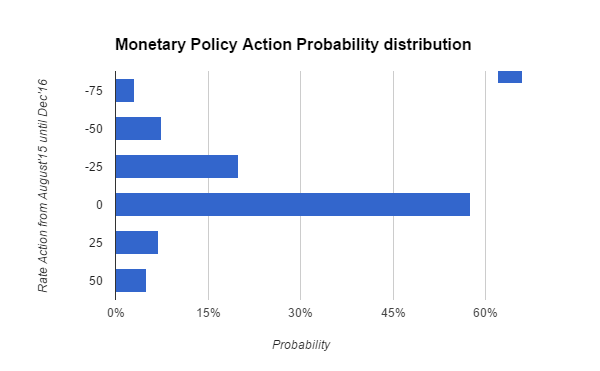

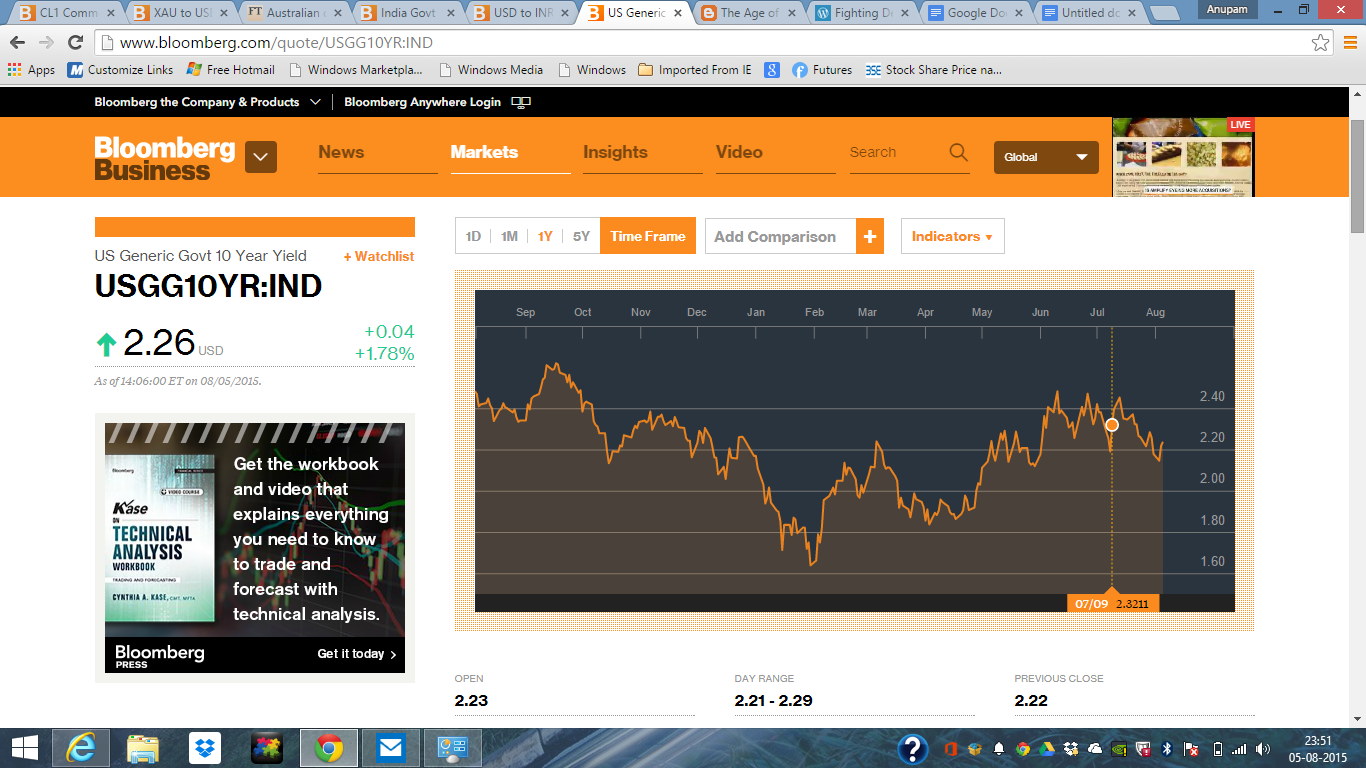

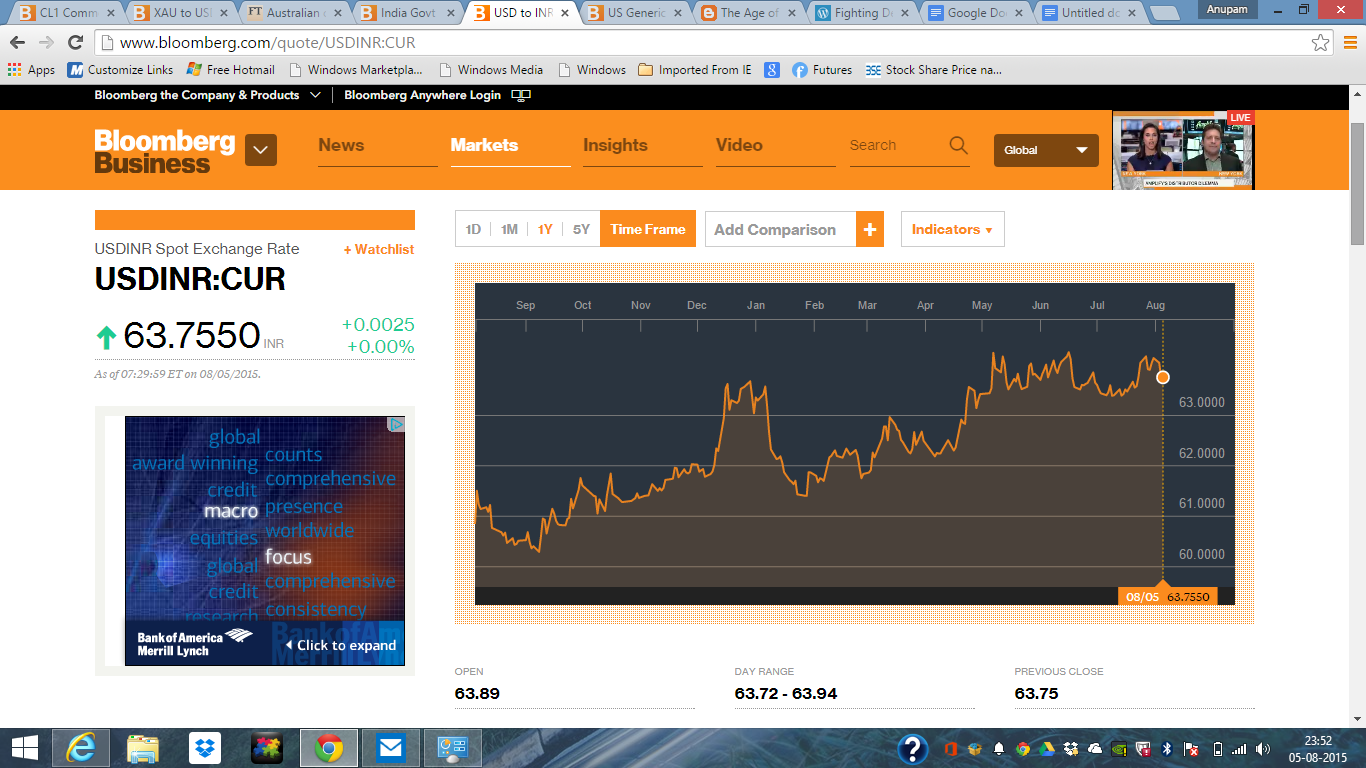

We had in a an earlier post (http://ageofdeflation.blogspot.in/2015/08/tantrum-not-us-fed-ahead.html) examined the chances of a USD,CNY and JPY carry trade unwind simultaneously as 1 in 31 and had cautioned that these odds are not so remote- all it needs is some senseless chores by guys with hands on monetary levers. And it has happened too soon for comfort. The US Fed seems hell bent on hiking rates at the same time when CNY and JPY carry trades are bursting. Now that's a sure recipe for disaster.

So what should Asian Central Banks do now that a simultaneous unwind of carry trades is in motion? Simple - ease monetary conditions domestically and let their respective currencies depreciate. Coupled with a possible weighing in of Govts' Fiscal support in the form of either Infrastructure investment or tax breaks for manufacturing and Services, the situation is imminently manageable.

And what should the US Fed, BoJ and PBoC be doing? Firstly, the US Fed should stop playing the pantomime with the public. Every kid in primary school knows that his/her dad earns a lot less than 8 years ago- a wage deflationary spiral. So notwithstanding the Obama jobs boom, the take-home pay is deflating as efficiency gains outstrip hiring effects. So the lack of inflation is not surprising and the Fed should stop behaving as though if a rate hike does not go through in September it would mean a major loss in credibility. Secondly, the PBoC should finally achieve the lower bound in its targetted monetary policy rates to beat off a very likely deflation over the next 3 - 6 months. Thirdly the BoJ has to stabilize the Yen and ensure that the JPY does not overly strengthen against the US$ in order not to crush off the yen carry trade with precisely the wrong synchronous effect. The watchword here is stability. Reduce volatility. If the market must go down, let it go down 2% in a day for 5 days, rather than 10% in 1 day.

Bad Bank/Good Bank

Now for some long term fixes- QUARANTINING of banking assets in Asian countries with pent-up credit booms now laid bare by an implosion into Non Performing Assets. The urgent need is for segregating banking assets into Good assets and Banking assets that have turned bad must be quarantined into a Bad Bank . It is important that there is a clear

demarcation of bad assets into the single "Bad Bank" which will have separate recovery targets and

capitalization. The rest of the "good banks" could only then function better with better credit targeting

and allocation without the haunting fear of the ghosts of the past which irrationally constrains credit /raises cost of credit even to deserving borrowers with clean records.

Government Investment into Non deflationary Infrastructure creation

In an era where every private entity is deleveraging, the State cannot also simultaneously deleverage.

To rationalize take a simple case: In a closed economy, where there are only two agents, you and

me, my spending is your earning and your spending is my earning. The entire world is a closed

economy. If everybody is deleveraging, if unemployment is high, wherefrom economic growth will

come? Hence the State has to invest in infrastructure such as Education, transportation, Tourism and the like that are inherently non-deflationary by borrowing at these historically low rates of sovereign bond yields.

After forceful public investment lifts the economy from the deflation, the private sector develops the

'animal spirits' to restart investment- borrowing and hiring picks up. In this stronger phase of economic

growth the private sector is more efficient than the public sector. Now here is where Keynes writings

did not resolve issues because he wasn’t around to witness the decadence of public enterprise in the

1970's in the US/UK, and indeed in much of the globe including the USSR. However it was getting

very obvious that in the 1970's, the size of the public sector was inefficient, gigantic and it was trying

to borrow money from the same public resulting in crowding out of the more efficient private sector.

The need of the hour then, was to cut down the size of the government and restrict the role of the

state to only those areas where no other actor could qualitatively contribute. That's where Reagan

and Thatcher came in, in the 1980's.

But this is 2015. The situation is different. We are entering a global deflation.

The only way out for a global recovery to gain ground is that Governments globally borrow massively and invest directly in the productive sectors of the economy. Roosevelt's "New Deal" needs to get

replicated and for that to happen we need to really ignore traditional thinktanks like the IMF that had

messed up in Latin America in the 80's and S.E. Asia in the late 90's and are now looking to repeat

the same errors in 2015.

Those who hold Reagan and Thatcher in great esteem can come in later, say in 2017, if by that time

the global economy has been safely pulled out of the woods, and the private sector is getting back its

mojo. By all means then-in 2017, dismantle the government and cut down upon activities that the private

sector can do better. There will be lethargy on either ends of the economic cycle. Functioning

democracies can tackle this type of lethargy and rent seeking on either ends of the cycle provided

institutions are allowed to function the way they ought to.